Balance Sheet

The Balance Sheet is a snapshot of what you own, what you owe, and what’s left over for the owner — frozen at a single moment in time. Three sections, one rule: Assets = Liabilities + Equity. If they don’t match, double-entry bookkeeping has been broken somewhere and the page below tells you where to look.

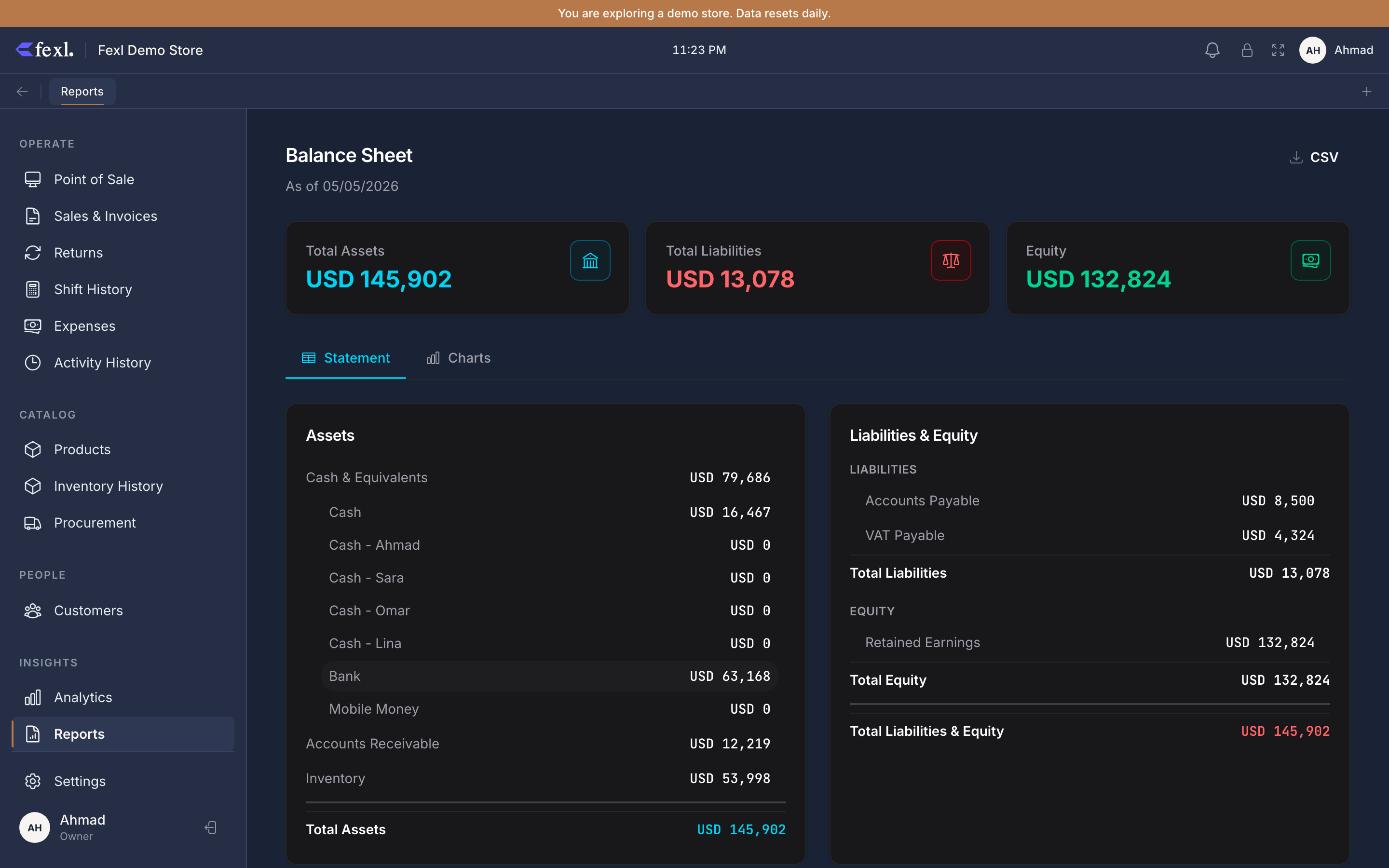

The header shows the as-of date — by default, right now. Pick an end date in the filter to ask “what did the books look like on 31 March?” Every figure on the page reads journal entries dated <= asOfDate, so the answer is reproducible: re-run the same date next year and you’ll get the same numbers.

Assets — what you own

Cash & Equivalents

The combined balance of every cash, bank, and mobile-money account at the as-of date. Computed as SUM(jel.debit) - SUM(jel.credit) over the journal-entry ledger for accounts whose code matches 1010, 1020, 1030, or any of their sub-accounts (1010-006, 1020-002, etc.). Click the row to expand the per-sub-account breakdown.

Accounts Receivable

Money customers owe you. Sums invoices.amount_owed for non-cancelled, non-comp invoices, plus customer opening balances. Account code 1100.

Inventory

The on-shelf value of your stock, valued by FIFO — open ingress layers’ qty_remaining multiplied by the per-unit cost stamped at restock. Account code 1200. See FIFO costing for how layers drain on each sale and how the cost on the balance sheet stays honest under price drift.

Total Assets

The sum of the three rows above. The cyan total at the bottom of the Assets card.

Liabilities — what you owe

Accounts Payable

Money you owe suppliers. Computed as max(opening_balance + (owed - paid), 0) per supplier, summed across the tenant. Account code 2010.

VAT Payable

Sales tax you’ve collected on customers’ behalf and owe to the tax authority. Sums invoices.vat_amount for non-cancelled, non-comp invoices. Account code 2020.

Commissions Payable

Delegate commissions earned but not yet paid out. Sums invoices.delegate_commission minus delegate-payment records. Account code 2030.

Customer Store Credit

Store credit you owe back to customers — refunds taken as credit, prepayments, gift cards. Sums the customer_credit_transactions ledger (credit adds, withdrawal subtracts). Account code 2100.

Total Liabilities

The sum of the four rows above. The red total under the Liabilities sub-section.

Equity — what’s left for the owner

Retained Earnings

Everything the business has earned and kept since day one — calculated here as Total Assets − Total Liabilities. This is the bookkeeping definition: whatever’s left after the creditors are paid is the owner’s.

The current period’s profit or loss flows into retained earnings the moment the journal entry posts — you don’t need to “close the books” to see it reflected here. For the period-by-period detail of how that profit was built, see the P&L report.

Why it must balance, and what to check if it doesn’t

The #56 fix in detail

Related

- Profit & Loss — where retained-earnings movement comes from

- General Ledger — line-by-line for any account on this page

- Trial Balance — the cheapest place to find an unbalanced JE

- FIFO costing — how the inventory line is valued

- Chart of Accounts — the meaning of each account code

- Release notes — v1.6.100 — bug #56